Every half year, BloombergNEF runs its Levelized Cost of Electricity (LCOE) analysis, a worldwide assessment of the cost competitiveness of different power generating and energy storage technologies – excluding subsidies.

Solar and Onshore Wind Leading as Cheapest Source of New Bulk Power

Contributed by | Bloomberg New Energy Finance

2H 2018 LCOE Update

Every half year, BloombergNEF runs its Levelized Cost of Electricity (LCOE) analysis, a worldwide assessment of the cost competitiveness of different power generating and energy storage technologies – excluding subsidies. These are the key, high-level results:

- Solar and/or wind are now the cheapest new source of generation in all major economies, except Japan. This includes China and India, where not long ago coal was king. In India, best-in-class solar and wind plants are now half the cost of new coal plants.

- The utility-scale PV market in China has contracted by more than a third in 2018 because of policy revisions in that country. This in turn has created a global wave of cheap equipment that has driven the benchmark global levelized cost of new PV (non-tracking) down to $60/MWh in 2H 2018, a 13% drop from the first semester of 2018.

- Our benchmark global levelized cost for onshore wind sits at $52/MWh, down 6% from our 1H 2018 analysis. This is on the back of cheaper turbines and a stronger U.S. dollar. Onshore wind is now as cheap as $27/MWh in India and Texas, without subsidy.

- In most locations in the U.S. today, wind outcompetes combined-cycle gas plants (CCGT) supplied by cheap shale gas as a source of new bulk generation. If the gas price rises above $3/MMBtu, our analysis suggests that new and existing CCGT are going to run the risk of becoming rapidly undercut by new solar and wind. This means fewer run-hours and a stronger case for flexible technologies such as gas peaker plants and batteries that do well at lower utilization (capacity factor).

- Higher interest rates in China and the U.S. over the past two years have put upward pressure on financing costs for PV and wind, but these have been dwarfed by lower equipment costs.

- In Asia-Pacific, more expensive gas imports mean that new-build combined-cycle gas plants with a levelized cost of $70-117/MWh continue to be less competitive than new coal-fired power at $59-81/MWh. This remains a major hurdle for reducing the carbon intensity of electricity generation in this part of the world.

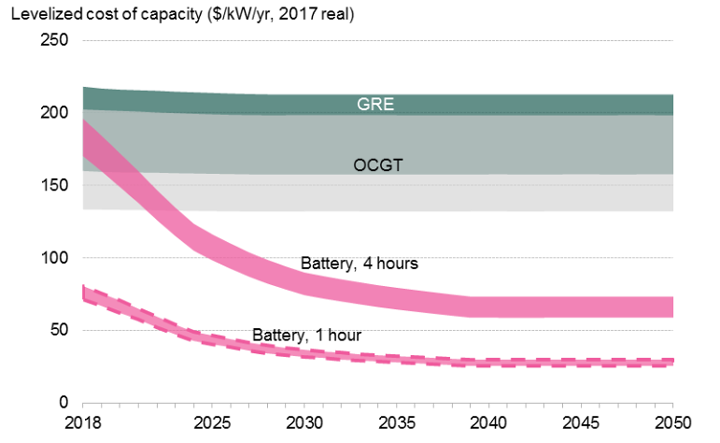

- Short-duration batteries are today the cheapest source of new fast-response and peaking capacity in all major economies except the U.S., where cheap gas gives peaker gas plants an edge. As electric vehicle manufacturing ramps-up, battery costs are set to drop another 66% by 2030, according to our analysis. This, in turn, means cheaper battery storage for the power sector, lowering the cost of peak power and flexible capacity to levels never reached before by conventional fossil-fuel peaking plants.

- Batteries co-located with PV or wind are becoming more common. Our analysis suggests that new-build solar and wind paired with four-hour battery storage systems can already be cost competitive, without subsidy, as a source of dispatchable generation compared with new coal and new gas plants in Australia and India.

BNEF’s 2H 2018 LCOE analysis covers nearly 7,000 projects across 20 technologies and 46 countries globally. All updated technology costs and performance inputs are available on BloombergNEF’s digital platforms.

Figure 1: Cost of new bulk and dispatchable electricity, China

Source: BloombergNEF.

Note: For thermal plants, the range captures a variety of capacity factors and costs and includes a carbon price in the case of coal and gas. For renewable-plus-storage systems, we assume a four-hour lithium-ion battery storage and the range captures the diversity of capacity factors in the country, as well as different capacity ratios between the storage and the generating asset (25%-100%). All LCOEs are unsubsidized.

Figure 2: Cost of new peaking capacity, Battery storage vs. gas peakers, China

Source: BloombergNEF.

Note: GRE: Gas reciprocating engine, OCGT: Open-cycle gas turbine. For gas peakers, the range captures a variety of capacity factors and costs. It includes a carbon price. For storage we assume lithium-ion batteries operating at a daily cycle, the range captures a diversity of financing costs and realized charging costs. All levelized costs are unsubsidized.

The content & opinions in this article are the author’s and do not necessarily represent the views of AltEnergyMag

Comments (0)

This post does not have any comments. Be the first to leave a comment below.

Featured Product