Merger and Acquisition information from Lincloln's Deal Reader.

Q3 2013 Deal Volume Comparison

Contributed by | Lincoln International

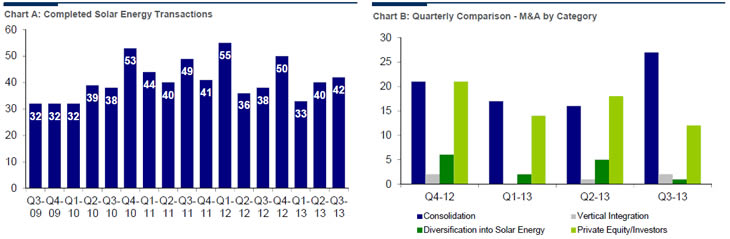

There were 42 completed solar energy transactions in Q3 2013 compared to 38 in Q3 2012. This represents an increase of 11% year over year, and continues the positive trend from the prior quarter. Consistent with the current quarter, the past seven quarters have averaged approximately 42 transactions each. Overall, this level of transaction activity is due to continued industry consolidation and private investment.

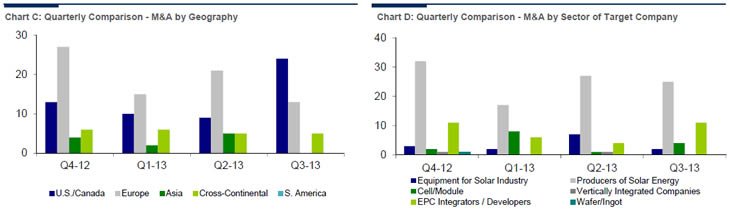

Within solar energy transaction activity, consolidation represented 64% of transactions, or 27 deals in Q3 2013. This is the largest share by any category in a quarter over the past several years. The next largest category was investment by private equity / investors with 12 transactions, or 29% of the Q3 2013 total. These top two categories continue to represent the vast majority of transactions in the solar market. Vertical integration reported two transactions, or 5% of the total, while diversification into the solar energy industry by corporations accounted for one transaction in the quarter. In Q3 2013, 57% or 24 of the 42 total transactions occurred in the U.S. / Canada region. This is more than double the first half of 2013 total for the region. Europe recorded 13 transactions or 31% of the total

in Q3 2013, which represented a smaller share of transactions than the previous quarter. Crosscontinental deals accounted for five transactions, or 12% of the total. Asia and South America did not record any transactions this quarter as activity was focused in other geographies.

In addition, there were 25 transactions for solar energy producers, or 60% of the total, which is in line with the total recorded in Q2 2013. This quarter there were 11 acquisitions for EPC integrators / developers, or 26% of the total transaction volume. There were four transactions for cells / modules producers, or 10% of total activity. Companies categorized as providers of equipment for solar accounted for two transactions, or approximately 5% of the Q3 2013 total. No transactions categorized as wafer / ingot producers or vertically integrated companies were recorded during the quarter.

Acquisition activity in Q3 2013 remained at levels consistent with recent history. Activity was significantly weighted to the solar markets in Europe and North America. Producers of solar energy continued to be the primary targets for acquisition, with the remaining balance of transactions fluctuating between the other categories. Regardless of target category, a large proportion of deals were the result of industry consolidation as smaller companies and projects are acquired by established players. The high level of consolidation activity highlights the maturation in the solar industry as companies look to build scale and grow their solar project portfolios through acquisition.

Margin Performance in the Solar Energy Industry

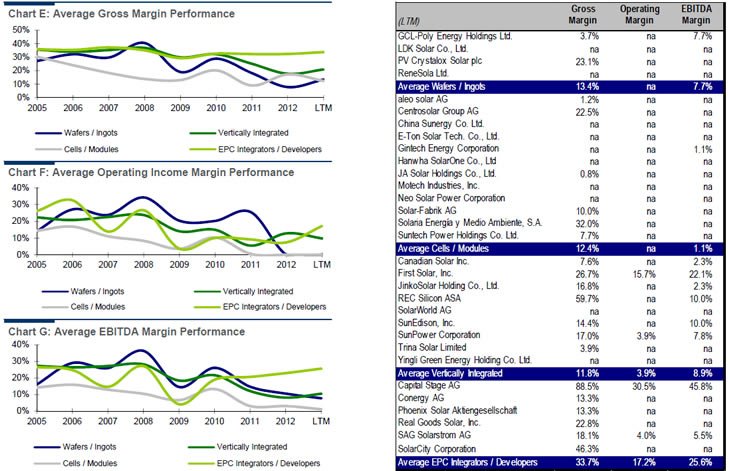

The changing dynamics in many global solar markets combined with continued declines in panel prices from a global oversupply have caused solar energy companies’ margins to decline across most sectors. However, certain sectors are now beginning to see slight margin improvements as consolidation and the continued industry shakeout helps companies improve operations and business focus.

The three graphs below provide an overview of gross margin, operating income margin, and EBITDA margin performance from 2005 through today. Each graph shows the margin performance by sector within the solar energy industry.

In terms of margin performance, vertically integrated companies saw improvement in gross and EBITDA margins in LTM Q3 2013, while operating margin exhibited a slight decline. The cells/modules and wafers/ingots companies generally saw declining margins across all measures since 2010. Finally, the EPC integrators/developers have had stable gross margins over the entire period, while operating and EBITDA margins trended upward from 2011 to LTM Q3 2013.

Overall, EPC integrators/developers had the highest margins in recent periods, followed by vertically integrated companies. On the other hand, cells/modules companies are exhibiting lower margins across all measures. Moving forward, further industry shakeout could help margin stabilization as well as the stabilization of solar panel prices.

Announcements

- ABB Ltd. (SWX:ABBN) acquired Power-One Inc. (July-13)

- First Solar, Inc. (NasdaqGS:FSLR) acquired a 1.5 GW project pipeline in the U.S. and Mexico from Element Power US, LLC (Aug.-13)

- M+W Americas acquired Gehrlicher Solar America Corporation from Gehrlicher Solar AG (Aug.-13)

- SolarCity Corporation (NasdaqGM:SCTY) acquired Paramount Energy Solutions (Sept.- 13)

Sources: All information contained in this article including the charts was obtained from company websites, Lincoln International’s internal data and Capital IQ.

About Lincoln International

Lincoln International specializes in merger and acquisition advisory services, debt advisory services, private capital raising and restructuring advice on mid-market transactions. Lincoln International also provides fairness opinions, valuations and pension advisory services on a wide range of transaction sizes. With fifteen offices in the Americas, Asia and Europe, Lincoln International has strong local knowledge and contacts in key global economies. The firm provides clients with senior-level attention, in-depth industry expertise and integrated resources. By being focused and independent, Lincoln International serves its clients without conflicts of interest. More information about Lincoln International can be obtained at www.lincolninternational.com.

Lincoln International specializes in merger and acquisition advisory services, debt advisory services, private capital raising and restructuring advice on mid-market transactions. Lincoln International also provides fairness opinions, valuations and pension advisory services on a wide range of transaction sizes. With fifteen offices in the Americas, Asia and Europe, Lincoln International has strong local knowledge and contacts in key global economies. The firm provides clients with senior-level attention, in-depth industry expertise and integrated resources. By being focused and independent, Lincoln International serves its clients without conflicts of interest. More information about Lincoln International can be obtained at www.lincolninternational.com.

The content & opinions in this article are the author’s and do not necessarily represent the views of AltEnergyMag

Comments (0)

This post does not have any comments. Be the first to leave a comment below.

Featured Product